In the world of accounting, two primary branches dominate the field: financial accounting and managerial accounting.

While both disciplines involve the processing and analysis of financial information, they serve distinct purposes and cater to different stakeholders.

Knowing how to distinguish and understand them is crucial for your career.

Table of Contents

Main Differences of Financial and Managerial Accounting

Here is a detailed analysis of the differences between the two accounting methods

Financial Accounting

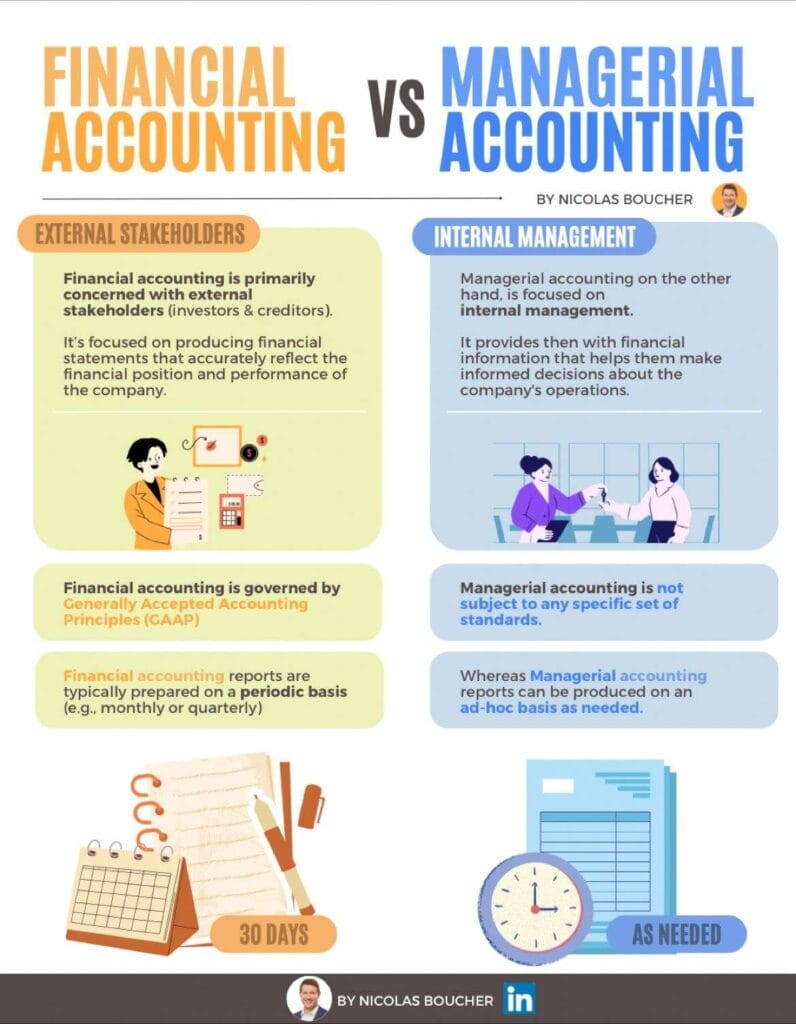

Financial accounting primarily focuses on providing accurate and reliable financial information to external stakeholders, such as investors, creditors, and regulatory bodies.

Its core objective is to prepare financial statements that reflect the company’s financial performance and position.

Key characteristics include:

- Producing financial statements (e.g., income statements, balance sheets, cash flow statements).

- Compliance with Generally Accepted Accounting Principles (GAAP).

- Ensuring transparency and accountability to external parties.

- Emphasis on historical data to assess past performance.

- Reports are prepared on a periodic basis (e.g., monthly, quarterly, or annually).

Managerial Accounting

Managerial accounting focuses on providing internal management with financial information to support decision-making and improve operational efficiency.

Its goal is to assist managers in planning, controlling, and evaluating the company’s activities.

Key characteristics include:

- Providing management with relevant and timely financial data.

- Flexibility in designing and implementing accounting systems.

- Facilitating budgeting, cost analysis, and performance evaluation.

- Emphasis on future-oriented information to guide strategic decisions.

- Reports can be prepared on an ad-hoc basis as needed (weekly, monthly).

Importance of Financial and Managerial Accounting

Financial accounting plays a crucial role in the following ways:

- Facilitating investment decisions: Accurate financial statements enable investors to assess the company’s financial health and make informed investment choices.

- Ensuring creditor confidence: Creditors rely on financial statements to evaluate creditworthiness and determine loan terms.

- Compliance with legal requirements: Financial statements are essential for meeting regulatory obligations and disclosing financial information to stakeholders.

Managerial Accounting: Managerial accounting offers several benefits to internal management:

- Strategic planning: Managers use financial data to set goals, develop strategies, and allocate resources effectively.

- Cost control and analysis: By monitoring costs, managers can identify areas of inefficiency, reduce expenses, and improve profitability.

- Performance evaluation: Comparing actual results with budgets and targets helps assess performance and take corrective actions.

- Decision support: Managers utilize financial information to evaluate alternative courses of action and make informed decisions.

Final Words

Both methods serve distinct purposes in the accounting realm.

Financial accounting focuses on reporting financial information to external stakeholders, while managerial accounting provides internal management with data for decision-making and performance evaluation.

While financial accounting adheres to established standards, managerial accounting offers more flexibility in designing accounting systems.

Both branches are integral to the success and sustainability of a company, offering valuable insights and enabling informed decision-making.

Do you want to use a modern tool to help you with your day-to-day accounting activities? Here you can unlock the power of ChatGPT for finance professionals and increase your productivity!

Key Takeaways

- Financial accounting caters to external stakeholders, while managerial accounting supports internal management.

- Financial accounting follows Generally Accepted Accounting Principles (GAAP), whereas managerial accounting does not have specific standards.

- Financial accounting emphasizes historical data, while managerial accounting focuses on future-oriented information.

- Financial accounting reports are prepared periodically, while managerial accounting reports can be produced on an ad-hoc basis.

- Both play vital roles in decision-making, performance evaluation, and strategic planning within organizations.