The manufacturing sector uses activity-based costing (ABC) most frequently because it improves the accuracy of cost data. Also, it is effective in identifying the expenses a firm incurs throughout the production process.

Therefore, here is everything you should know about activity-based costing if you are a finance professional.

Table of Contents

Definition of Activity-Based Costing

Activity Based Costing (ABC) is a cost accounting method.

ABC is a method of assigning costs to products or services based on the specific activities or resources that are consumed in their production or delivery. Also, it is an alternative to traditional costing methods, such as job costing or process costing, which assign costs based on a more general allocation of overhead costs.

Specificities

In traditional cost accounting, overhead costs are allocated using only one arbitrary rate. But, ABC allocates the overhead more accurately.

How?

By arranging overhead activities in cost pools.

Cost pools

A cost pool is a group of costs either based on the following:

- a cost center,

- a group of cost centers or

- a measurable activity (measured as a % of the total time spent by a group of people).

For example, cost pools can be:

- Warehouse management

- Customer service

- Maintenance

- R&D

- Technical training

- Warranty costs

Measures

After defining cost pools, you need to define the unit measures. Additionally, you will use the unit measures to allocate the cost pools to the products.

For example, unit measures can be:

- number of units produced

- number of orders

- amount of material used

- percentages

- square meters used

Advantages and disadvantages of the Activity-Based Costing Method

Pros

- More Accurate

- Also, you can use multiple rates

- Yet, a better view of the profitability of a product

- Furthermore, it can help reduce the structure cost by choosing activity having a heavy impact on product cost

Cons

- Difficult to implement

- In addition, you can not use it for external reports as you mix COGS and SGA in the product costs

- Needs to have the right level of details

- Moreover, needs consistency of the methods

- Overhead costs not directly allocated

Case study

#1: Let’s imagine a manufacturing company called “TOP DESK.” They produce desks for offices. They have two products: a standard desk and an electric standing desk.

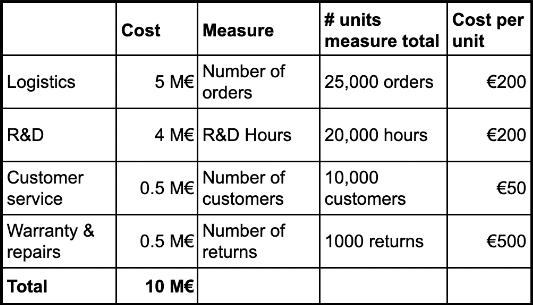

#2: They have 10M€ overheads related to the products:

- Logistics: 5M€

- R&D: 2M€

- Customer service: 2M€

- Warranty & repairs: 1M€

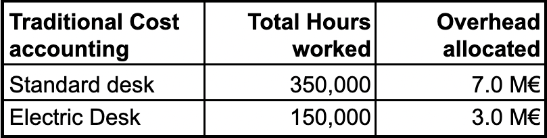

#3: Traditional cost accounting:

Overhead is allocated to each direct hour. Let’s say there are 500,000 direct hours worked.

- 10,000,000€ / 500,000 = 20€ overhead per hour

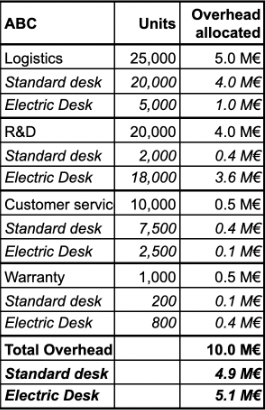

#4: Activity-Based Costing accounting:

#5: Comparison:

Traditional Cost accounting: overhead allocated based on total direct hours worked for each product.

#6: Comparison: ABC: overhead allocated based on activity:

#7: Conclusion:

Finally, having a more accurate overhead allocation method helped improve the transparency of the profitability of each product.

The case study I presented here shows how two different products can have different profitability based on the type of cost accounting you use.

On the one hand, in traditional cost accounting, the electric desks had a lower overhead allocation as the allocation was based on the number of direct hours used to produce electric desks.

On the other hand, in the ABC method, the allocation was more precise and accounted for the fact that electric desks used more R&D and warranty costs than the standard desks due to their complexity. As a result, the electric desks were less profitable using the ABC method than using traditional cost accounting.

Critics of The Activity-Based Costing Method

However, like everything in Finance, ABC is not the perfect method that fits all businesses (see cons). Additionally, some other methods allocate the overhead directly to specific activities.

The Bottom Line

To sum up, use this method when you have difficulties understanding the profitability of your products and you notice that using an arbitrary overhead allocation key penalizes or favorite too significantly one product.

Then, make sure you use this information for your Go-To-Market Strategy in order to maximize the profit of the business based on its resources.

Also, if you want to receive more finance tips like this, feel free to sign up for my newsletter. If you subscribe, every week, you will receive an email from me where I share best practices, career advice, templates, and insights for Finance Professionals.